Research

The world is reeling under the impact of the coronavirus pandemic. Its devastating damage to humans, its influence over our daily interactions, and its economic consequences are all too clear. Financial and medical crises could go hand in hand as a rise in unemployment and reduced access to healthcare could lead to adverse health outcomes. This has required concerted policy actions from global fiscal and monetary policy authorities to cushion the adverse economic consequences related to the outbreak.

For investors, the pandemic has created an unusual level of risk, causing investors to suffer considerable loses in a very short period of time. The spread of the virus has triggered panic across the world and soured investors sentiment. Amid the prevalence of the coronavirus, concerns about economic growth have intensified and equity markets have suffered steep pullbacks. A mix of deep uncertainty regarding the impact of the coronavirus on the one hand and the ability of policymakers to counter that threat on the other, poses a challenge.

As infections begin to peak in many countries, concerns are mounting among investors about Africa’s under-testing and under-reporting of COVID-19 cases. This has intensified uncertainty about the performance of investments in Africa, especially portfolio investments in African financial markets, generating pandemic-induced volatility.

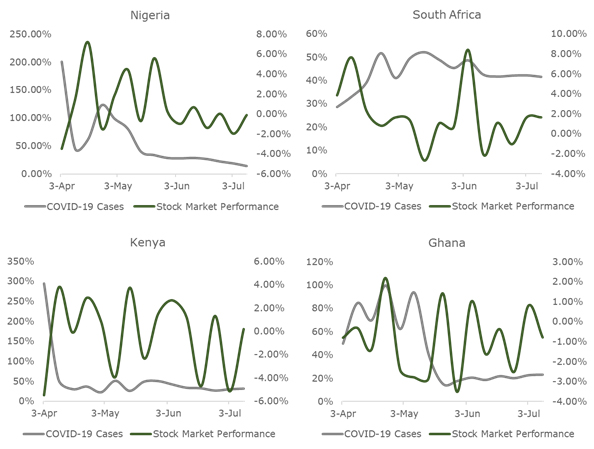

Stock Market Volatility vs COVID-19 Incidence Rate of select SSA countries (%)

Sources: Bloomberg, Humanitarian Data Exchange, Vetiva Research

The impact of the coronavirus outbreak on financial markets across the SSA sub-region has been somewhat mixed. While uncertainty related to the coronavirus-pandemic has had a negative impact on the volatility of Ghana and Kenya’s markets (Correlation: -0.92 & -0.24 respectively), the effect on South Africa and Nigeria’s stock markets has been largely positive (Correlation: 0.70 & 0.63 respectively) in spite of their higher case incidence. Similarly, the Kenyan and Ghanaian stock markets have continued to experience a high level of volatility in spite of their fairly stable rate of contamination over the past few weeks while the degree of volatility within the Nigerian and South African stock markets has moderated with the steady rates of contamination both countries have recorded over the past few weeks.

With concerns of a more severe second-wave and economic growth projections looking dismal, investors in the SSA region need to be extra cautious because volatility can often be as virulent as a virus. Although we expect investor sentiment to improve somewhat in the coming months as countries flatten the COVID-19 curve, that is not to say there isn't also a risk of the coronavirus impact being bigger than currently anticipated. Rising tides may lift all boats, but falling tides could wash away market gains much faster. As such, times like these require a steady hand holding on to your investments and judiciously buying when there are opportunities. And THERE ARE opportunities, though a lot longer term.

Stock Market Comparables (as at 15th July 2020)

| Country | P/E | P/B | P/S |

|---|---|---|---|

| Brazil | 37.8 | 2.2 | 1.4 |

| Japan | 28.0 | 1.8 | 1.1 |

| South Korea | 26.1 | 0.9 | 0.6 |

| India | 24.0 | 2.7 | 2.5 |

| UK | 22.7 | 1.5 | 0.9 |

| Taiwan | 21.1 | 1.9 | 1.1 |

| EU | 21.1 | 1.6 | 1.2 |

| US | 20.2 | 4.0 | 2.0 |

| South Africa | 17.6 | 1.7 | 1.4 |

| China | 17.2 | 1.6 | 1.2 |

| Indonesia | 16.8 | 1.4 | 1.4 |

| Nigeria | 8.0 | 1.2 | 1.0 |

| Kenya | 7.8 | 1.3 | 1.4 |

| Ghana | n/a | 1.6 | 1.1 |

Sources: Bloomberg, Vetiva Research

From a comparables perspective, SSA stocks are considerably cheaper now compared to stocks in many non-African developing economies and advanced economies. This suggests that the region has potential to deliver much higher returns on portfolio investment than other economic regions, as soon as global risk sentiment improves with increased clarity on the coronavirus pandemic. But emphasis should be placed on caution because the pandemic evolution and economic recovery view remain uncertain.