Recently, the Macro Desk of Vetiva Research released its Macroeconomic Outlook for FY’23,

titled Riding the Seesaw.

Below is a summary of our outlook:

Geopolitics: Skipping downhill

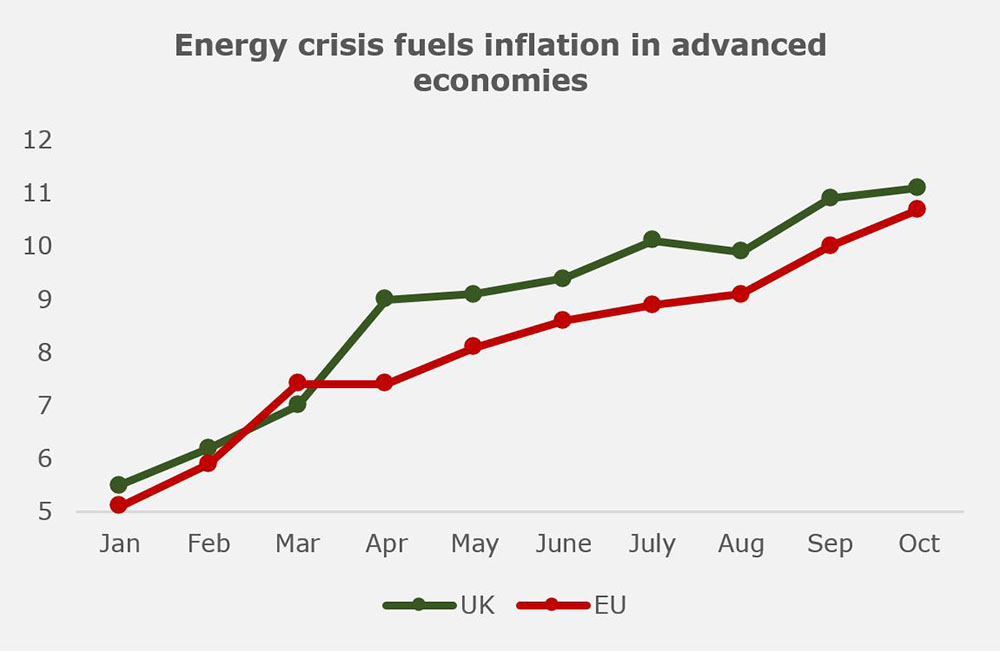

Monetary policy tightening, the energy crisis, and COVID restrictions are all expected to contribute to a global slowdown in 2023.

While monetary policy tightening may stifle growth in the United States, growth in the Eurozone may be hampered by the energy crisis.

In Asia, China's property crisis and continued COVID controls may dampen real output.

In July 2022, a deal (Black sea grain deal) was signed between Ukraine and Russia to resume grain and fertilizer exports

from three key Black Sea ports -Odesa, Chornomorsk, and Yuzhny - provided some relief to food prices. To combat multi-year high inflation,

policymakers have raised interest rate to record-levels. This stance could be sustained unless geopolitical tensions ease in 2023.

Source; FAO, Vetiva Research

Elections and Enumerations

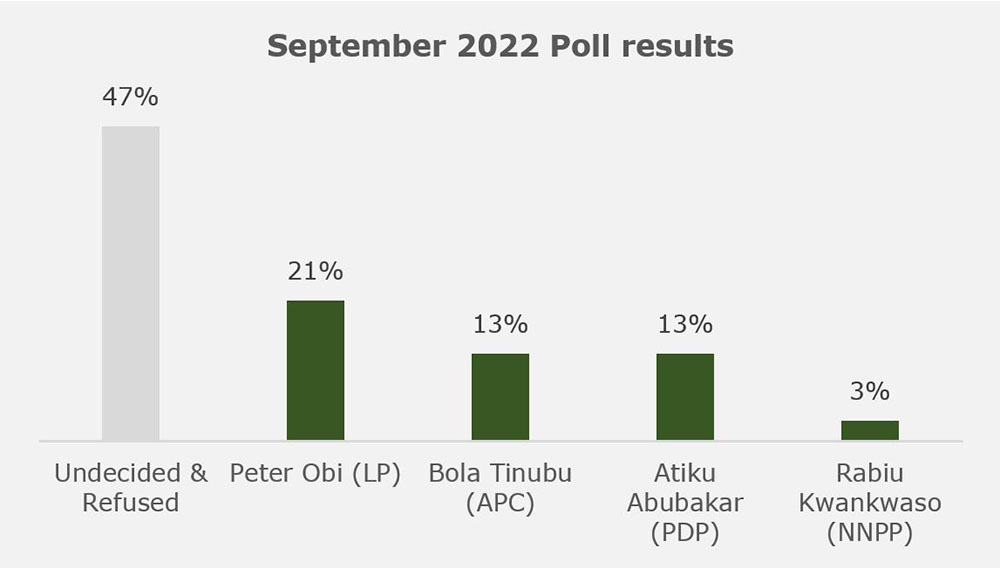

With the incumbent President Muhammadu Buhari signing out in 2023, the upcoming elections could shape the Nigerian economy

for the next four (to eight years). Developments leading up to the election reveal one clear fact – the outcome of the Presidential

election is too close to call and makes policy outlook hazy. Of the 14 contenders for the top job, NOI polls streamlined the number

of popular candidates to four - Peter Obi of the Labour Party (LP), Asiwaju Bola Ahmed Tinubu of the

All Progressives Congress (APC), Atiku Abubakar of the People's Democratic Party (PDP), and Rabiu Kwankwaso of the New Nigeria

People Party (NNPP). The poll was, however, unable to predict a clear frontrunner as the undecided respondents and those who preferred not to reveal

their candidate summed up to 47% of respondents (2019 polls: 38%). With most of the leading candidates in favour of pro-market policies,

this could induce the implementation of the needed reforms to steer the economy in the right direction.

Source; ANAP, NOIPolls

Real Sector outlook: Still on the verge of growth

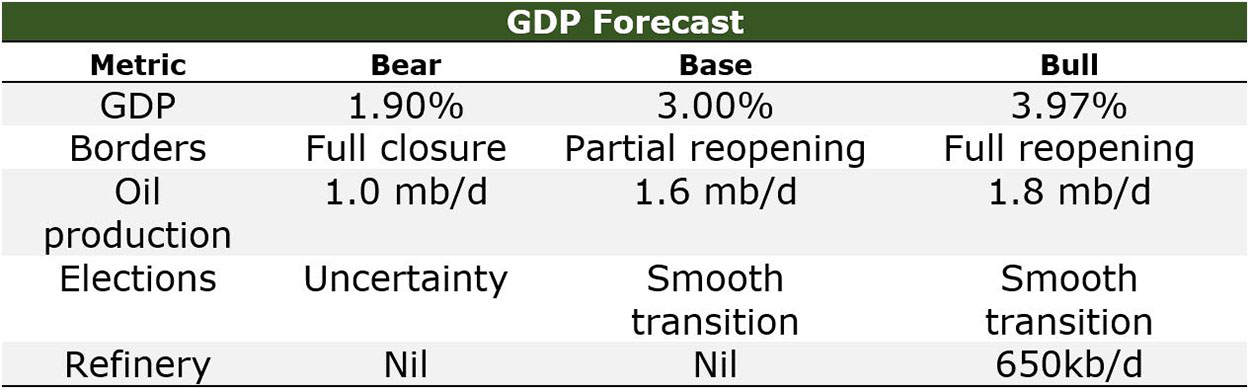

In 2023, we expect the overall economy to expand by 3.0% y/y. This positive outlook is hinged on sustained recovery in

the oil sector amid a moderation in non-oil growth. The oil sector, which has been in a three-year recession,

is expected to rebound in 2023. We base our optimism on effective pipeline surveillance and the clampdown on

illegal connections to the Trans-Forcados terminal. We also see consolidated gains from the newly commissioned

Amukpe-Escravos Pipeline. Our bull estimate of 3.97% is hinged on the commencement of domestic refining and other oil exploration activities.

Source: NBS, Vetiva Research

Fiscal policy: Who will bell the cat?

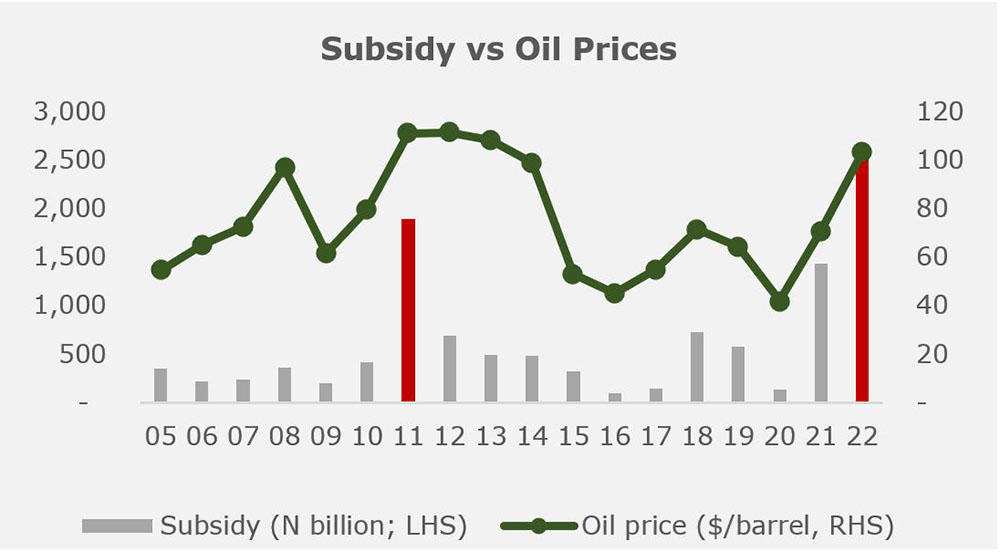

The 2023 budget proposal of ₦20.5 trillion is 21% larger than the 2022 appropriation act. The larger budget figure is driven

by a higher debt service provision (₦6.6 trillion; +69% y/y) and non-debt recurrent spending plan (₦8.3 trillion; +20% y/y) while

allocation to capital projects was lower than the 2022 appropriation act (₦4.9 trillion; -10% y/y). On the revenue leg, the government

plans to generate ₦9.7 trillion in revenue (-4.0% y/y) after a subsidy bill of ₦3.0 trillion is deducted. The federal government’s

intention to phase out subsidies in the second half of 2023 could pave the way for fiscal sustainability alongside oil production recovery.

However, the target date (June 2023) for removal doubles as the handover date of the incumbent administration. Given the unpopular

but necessary decision to expunge fuel subsidies, this begs the question – who will bell the cat?

Source: NEITI, Macrotrends, Vetiva Research

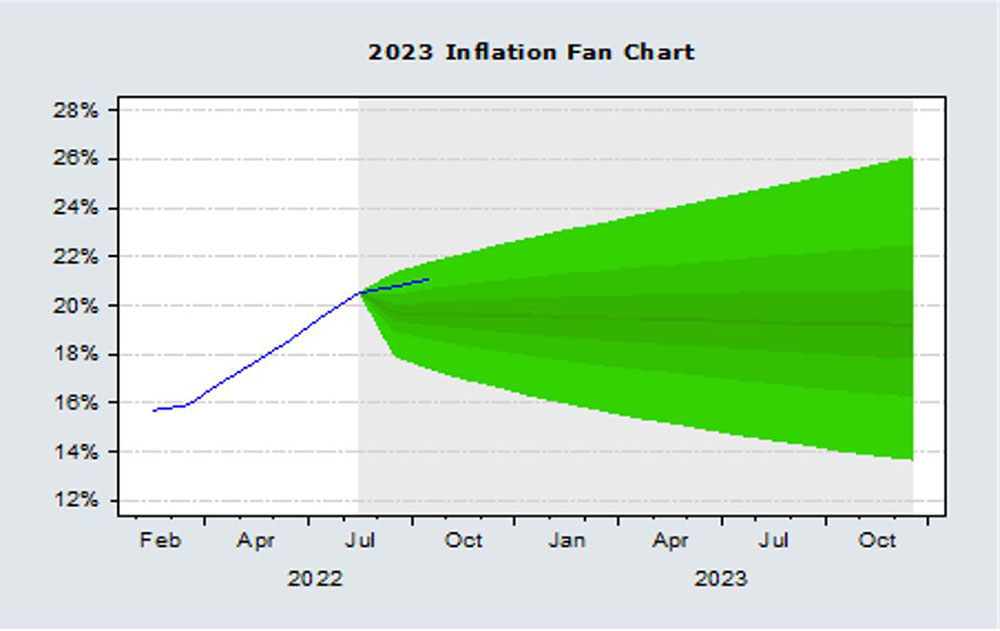

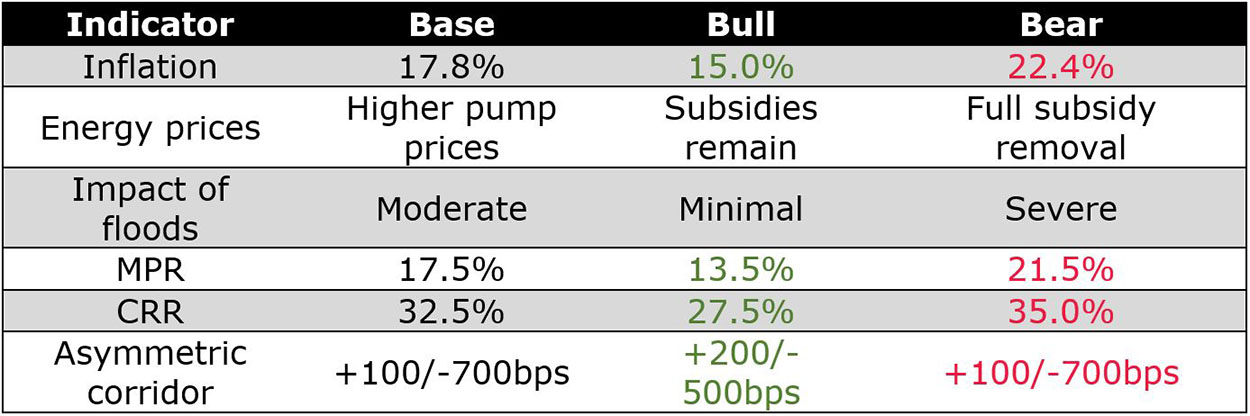

Inflation: Uncertainties cloud outlook

In 2023, current information suggests inflationary risks are tilted to the upside. While we assign more weight to the impact of floods

and other disruptions on inflation, the subsidy removal debate remains a key determinant of the direction of inflation in 2023. Given the

high uncertainty around the possibility of full subsidy removal, we adopt a scenario approach to guide our FY’23 inflation expectations.

Given this backdrop, inflation outlook is split into two halves. Due to the prior year’s high base, headline inflation could trend downwards in

the first half of the year (H1’23). The outlook for H2’23 is tilted towards the upside, as both subsidy and flooding constraints

send consumer price inflation higher. Given the upside risks, we expect headline inflation to average 17.80% y/y (2022E: 18.83%).

For our bear case scenario, the full removal of subsidies to 22.14% y/y) in 2023.

Source: EViews, Vetiva Research

Monetary Outlook: Subsidy removal could guide interest rate direction

In 2023, monetary policy decisions may be influenced by the decision on fuel subsidies, pressures on the global supply chain,

and major central banks' monetary policy actions. Due to the belief that inflation may soon reach a peak, the central bank

may raise rates more slowly in the first half of the year. However, if the next administration decides to eliminate subsidies as

is anticipated in H2'23, inflation may increase further, which may result in further rate hikes.

Source: Vetiva Research

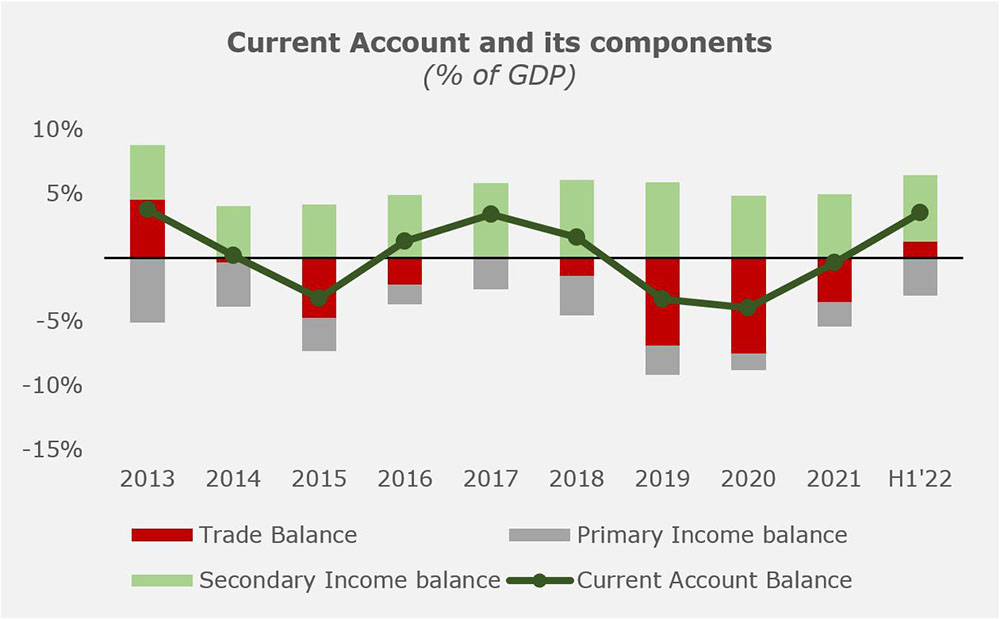

External Outlook: FX Gap widens despite positive net trade flows

In Q2’22, Nigeria’s current account position grew by 92% q/q to $5.1 billion (4.7% of GDP). This improvement was driven by higher goods

account surplus (net exports), a thinner net income account deficit (investment income) and a lower transfer account surplus (remittances).

The gains from these sub-accounts surpassed the services account deficit (majorly transport and travel).

In terms of trade, rising oil prices caused exports to increase by 5% q/q to $18.2 billion. Meanwhile, imports fell by 10% q/q to $12.5

billion, leaving a net merchandise balance of $5.7 billion.

In August 2022, the Federal Government awarded a pipeline surveillance contract to Government Ekpemupolo (Tompolo). The contract yielded positive

results within a short timeframe as several illegal connections and pipelines were discovered. The removal

Source: CBN, Vetiva Research

of these illegal connections and the completion of repairs on the Trans-Forcados pipeline are

triggers for higher oil production over the near term. Thus, we expect higher goods account surpluses.

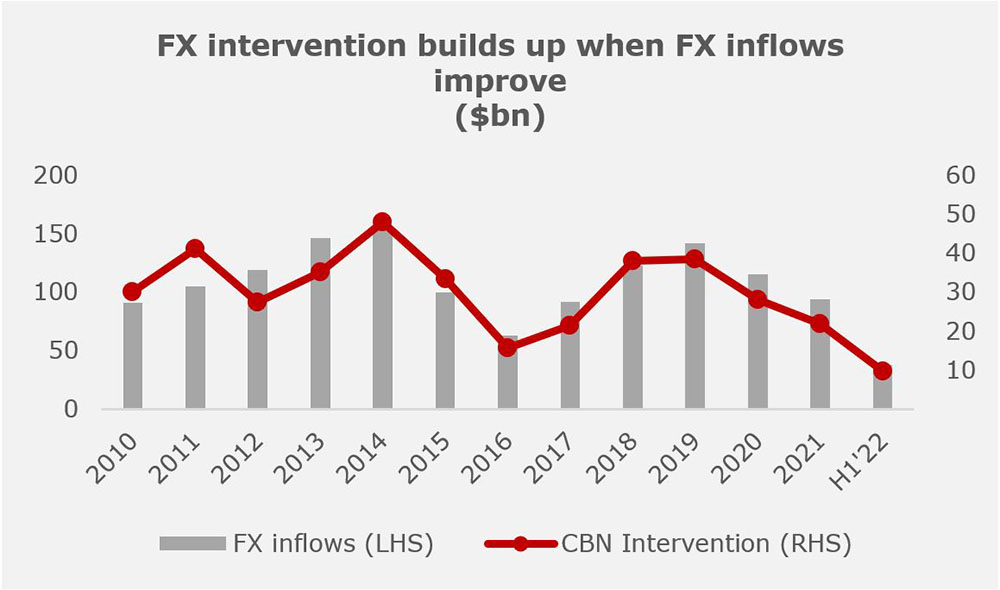

FX Outlook: Pipeline surveillance could buoy the Naira

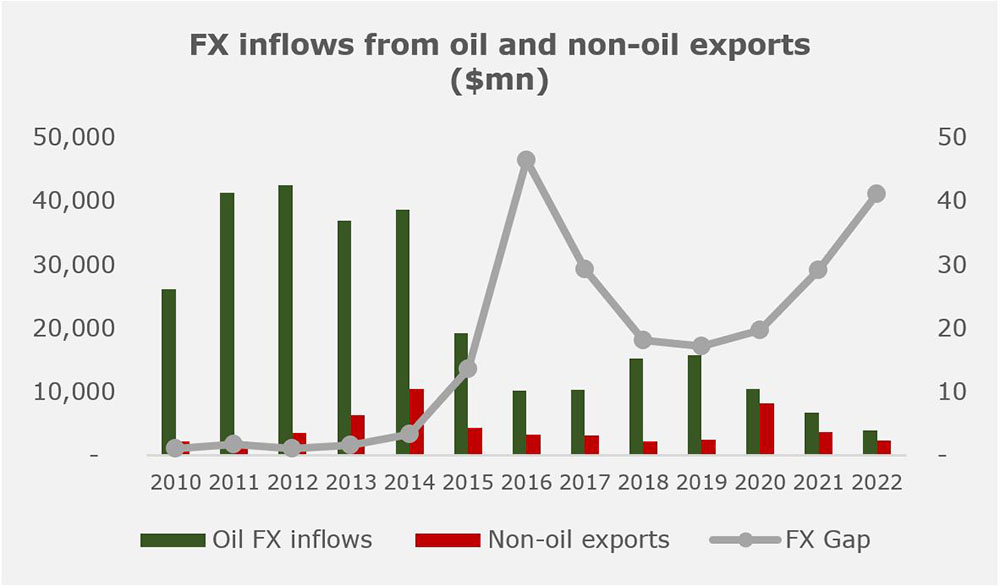

Amid the descent in oil earnings, the apex bank has made moves to de-risk Nigeria’s FX inflows from the vagaries of the oil sector.

Thus, it introduced the RT200 FX programme, which seeks to improve non-oil export flows into the country.

The program aims to raise $200 billion in non-oil FX earnings over the next 3 to 5 years. Although the program yielded an

FX inflow of $4.9 billion in 2022 (+56% y/y), the historical contribution of non-oil exports to foreign exchange flows is still low (c.4%).

While the absolute contribution of the oil sector has waned from an annual inflow of $38 billion in 2014 to an annual inflow of $6 billion

in 2021, we expect increased crude receipts and higher foreign exchange earnings in 2023. However, we note that a substantial

reduction/total elimination of fuel subsidy is necessary to boost FX inflows into the reserves.

Source: CBN, Vetiva Research

Our prognosis going into 2023 suggests that the Naira’s performance hangs largely on higher oil production receipts and improved

intervention in the foreign exchange market. Thus, should our baseline scenario of stronger oil production and a reduced

subsidy bill play out, we expect increased foreign exchange inflows and a narrower FX gap. We had established in our H2’22 Outlook

that the Naira is undervalued in the parallel market, though slightly overvalued in the official market. Thus, while we see the Naira

slipping to ₦480/$ in the official window, our base estimate for the parallel market is hinged on an appreciation to ₦665/$ in 2023.

Source: CBN, Vetiva Research